🙃 Stocks go down. Bonds go down. Bitcoin goes down.

HGP Newsletter #8

👋🏼 Hello wealth builders! Why are you receiving this? You want to be in a good place financially. This is where I share educational content and practical tips on personal finance, so you can get to your good place, wherever that maybe.

Welcome to the 8th issue of the hellogoodplace (HGP) newsletter.

What I’ve been up to:

🇰🇷 안녕하세요 (hello) from Seoul!

Although I visit Seoul every year, I usually visit during Winter. The weather here is akin to New York, so Winters are awful but it’s just about perfect during the Spring. I unfortunately missed the cherry blossoms this year so I’ll have to be here earlier next year.

🇨🇦 BrightPlan

If you thought traveling in a new country is intimidating, try launching a product there! BrightPlan is now available for Canadian employees as of this week. It was a ton of challenging work, but working on something that nobody has tried before is the exact reason I joined BrightPlan. I also learned more about Canadian personal finance than I ever thought I needed to know :)

Market Update

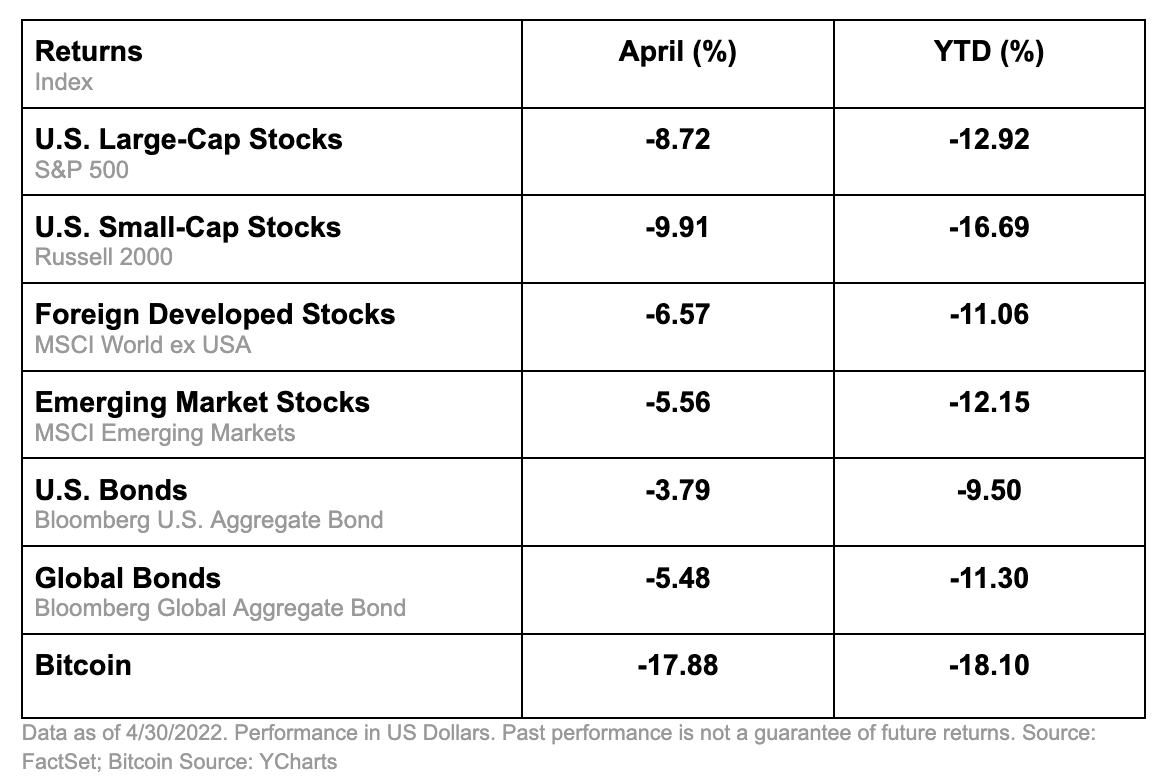

After teasing us in March with a slight uptick, the stock market took a sharp turn lower in April. The S&P 500 fell almost 9% this month and is down close to 13% for the year. That puts the US market in correction territory (down 10%), but not yet in recession territory (down 20%). US small stocks declined almost 10%, and tech stocks took a beating dropping 13%. That was the biggest one-month decline for tech stocks in more than 10 years. Foreign stocks fared better on relative terms. Developed foreign stocks fell 6.57% while emerging markets stocks lost 5.56% in April. With continuing concerns over the highest inflation rate in 41 years, lingering supply chain challenges, and the Russia/Ukraine conflict, don’t expect volatility to ease anytime soon.

US bonds fell 3.79% for the month as investors expect the Fed to continue aggressively tightening monetary policy. US bonds are down almost 10% so far this year. With the S&P 500 down almost 13%, that puts US stocks and bonds on track for their biggest simultaneous drop going back to 1976. Global bonds fell 5.48% for the month, and over 11% for the year, as Europe is also experiencing record high inflation at 7.5%.

Various Flavors of Risk

There are several types of risk that you should consider for your investment strategy. Among them:

Risk Capacity is your ability to take risk based on your situation. In general, long-term goals have high risk capacity and can afford to hold more risky assets, such as stocks. That’s because the longer the time horizon, the more likely stocks will provide a positive return. Shorter-term goals have less ability to take risk and therefore should hold more cash and bonds.

Risk Tolerance is your ability to stomach risk based on your emotions and it is more difficult to measure. Market volatility and downturns provide a great opportunity to reassess your risk tolerance. That’s because imagining a 10% drop in your portfolio is very different from actually going through it. Market volatility is uncomfortable, but it shouldn’t be so uncomfortable that you to lose sleep at night. If the recent market volatility is causing a high level of stress, you might be taking on more risk than you can emotionally handle.

Purchasing Power Risk is the risk of inflation eating away at your savings, and should be closely balanced with your risk tolerance. For example, cash does not go up and down like stocks and bonds, and therefore can feel like a safer asset. But that depends. For a short-term goal of buying a new computer next month, it would be a safe asset. For a long-term goal of retiring if 20 years, putting it in cash would be safe from volatility but not from inflation. For more on protecting your assets from inflation, here is a link to my last issue on inflation.

This chart only goes up to 2012, but the direction of these returns won’t change much through 2021. In fact, it probably would look worse given stocks had a great decade while cash basically paid nothing. Holding cash for long-term goals is a recipe for a slow and consistent demise of your purchasing power.

When constructing your portfolio, first think about what goal you want it to accomplish. Then assess the three level of risks to come to an appropriate asset allocation (stocks/bonds/crypto). This is how I’ve approached managing millions of dollars for my clients and it’s worked for decades, and it’ll work for you.

To being in a good place,

Daniel

hellogoodplace.com

Twitter: @profdlee

Instagram: @hellogoodplace

Youtube: Monday Monday with Prof DLEE

Source:

Market beat T-Bills

Market is Fama/French Total US Market Research Index. T-Bills is One-Month US Treasury Bills. There are 1,027 overlapping 10-year periods, 1,087 overlapping 5-year periods, and 1,135 overlapping 1-year periods.

Cash Has Provided a Negative Real Return, After-Tax Return.